All Categories

Featured

Table of Contents

That normally makes them a more inexpensive choice for life insurance protection. Some term policies may not keep the costs and death benefit the exact same over time. You do not wish to incorrectly think you're acquiring level term protection and afterwards have your death benefit change later. Many individuals obtain life insurance coverage to aid economically safeguard their loved ones in instance of their unexpected fatality.

Or you may have the choice to convert your existing term coverage right into an irreversible plan that lasts the remainder of your life. Various life insurance policy policies have prospective benefits and disadvantages, so it is necessary to understand each before you determine to purchase a plan. There are numerous advantages of term life insurance policy, making it a popular choice for insurance coverage.

As long as you pay the costs, your beneficiaries will get the death benefit if you die while covered. That said, it is essential to note that the majority of policies are contestable for two years which suggests protection can be rescinded on fatality, needs to a misstatement be found in the app. Policies that are not contestable typically have a graded death benefit.

Premiums are normally reduced than whole life policies. With a degree term policy, you can select your insurance coverage amount and the policy size. You're not locked right into a contract for the rest of your life. Throughout your plan, you never ever have to stress over the costs or survivor benefit quantities altering.

And you can not squander your plan throughout its term, so you won't obtain any financial gain from your past protection. Similar to various other sorts of life insurance policy, the price of a level term plan relies on your age, coverage requirements, employment, lifestyle and wellness. Normally, you'll locate much more budget-friendly protection if you're more youthful, healthier and less risky to insure.

Cost-Effective Decreasing Term Life Insurance

Considering that level term premiums stay the same for the duration of coverage, you'll understand specifically how much you'll pay each time. Degree term protection likewise has some adaptability, enabling you to customize your plan with added features.

You may have to meet specific conditions and qualifications for your insurer to pass this motorcyclist. On top of that, there might be a waiting duration of up to six months prior to working. There additionally might be an age or time frame on the coverage. You can include a child motorcyclist to your life insurance policy so it likewise covers your children.

The fatality benefit is normally smaller, and protection typically lasts until your child turns 18 or 25. This biker might be a much more cost-effective method to assist guarantee your youngsters are covered as motorcyclists can commonly cover multiple dependents at the same time. Once your kid ages out of this protection, it may be possible to convert the motorcyclist into a new plan.

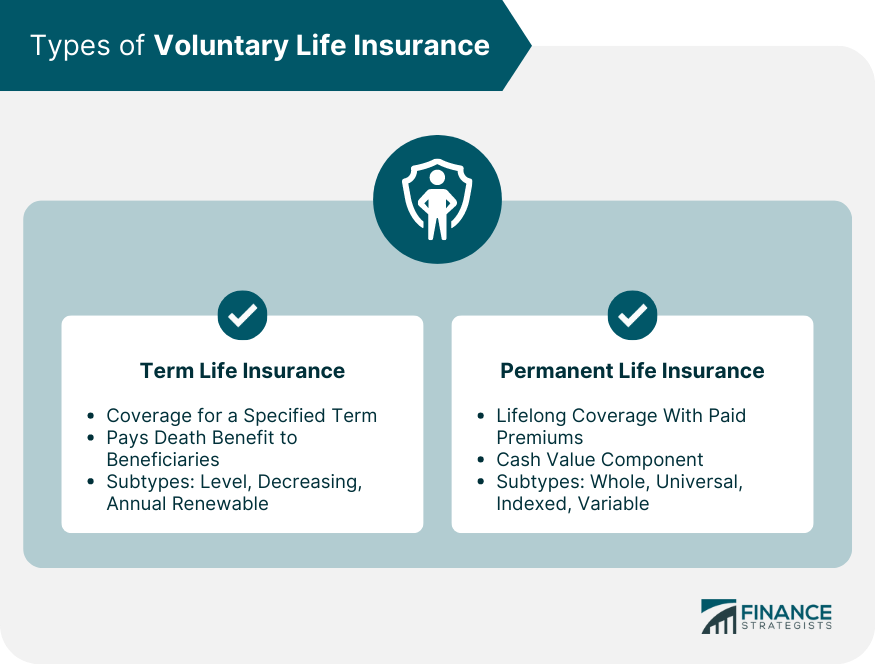

The most typical kind of long-term life insurance policy is entire life insurance coverage, yet it has some key differences compared to degree term insurance coverage. Here's a standard summary of what to consider when contrasting term vs.

Affordable Term 100 Life Insurance

Whole life entire lasts for life, while term coverage lasts insurance coverage a specific period. The premiums for term life insurance coverage are typically reduced than whole life protection.

Among the main functions of level term insurance coverage is that your costs and your survivor benefit do not change. With lowering term life insurance, your premiums remain the very same; nevertheless, the survivor benefit amount gets smaller sized with time. For instance, you might have insurance coverage that starts with a survivor benefit of $10,000, which might cover a mortgage, and after that annually, the fatality benefit will certainly reduce by a collection quantity or percentage.

As a result of this, it's usually a much more budget friendly kind of level term coverage. You might have life insurance policy through your employer, but it might not be enough life insurance policy for your requirements. The very first step when purchasing a plan is figuring out exactly how much life insurance coverage you require. Consider elements such as: Age Household size and ages Work condition Income Financial debt Lifestyle Expected last expenditures A life insurance calculator can help establish just how much you require to begin.

After choosing on a policy, complete the application. For the underwriting process, you might have to provide basic individual, health and wellness, way of living and work information. Your insurance firm will certainly determine if you are insurable and the threat you may offer to them, which is shown in your premium costs. If you're approved, sign the documentation and pay your very first premium.

Does Term Life Insurance Cover Accidental Death

Consider organizing time each year to assess your policy. You might wish to update your beneficiary information if you've had any type of significant life changes, such as a marriage, birth or separation. Life insurance policy can often really feel complicated. You don't have to go it alone. As you explore your options, consider discussing your demands, desires and worries about a monetary professional.

No, level term life insurance coverage doesn't have cash money value. Some life insurance policy policies have an investment feature that permits you to build cash worth in time. A section of your premium repayments is alloted and can earn interest in time, which expands tax-deferred during the life of your coverage.

These plans are typically significantly much more costly than term coverage. If you get to completion of your plan and are still alive, the coverage ends. Nevertheless, you have some options if you still want some life insurance policy coverage. You can: If you're 65 and your insurance coverage has gone out, for instance, you might want to buy a new 10-year level term life insurance coverage plan.

Level Term Life Insurance Meaning

You might be able to transform your term protection into a whole life plan that will certainly last for the rest of your life. Numerous sorts of degree term plans are convertible. That indicates, at the end of your insurance coverage, you can convert some or all of your policy to whole life protection.

Level term life insurance coverage is a policy that lasts a set term typically in between 10 and 30 years and features a degree death benefit and level premiums that remain the very same for the entire time the policy holds. This indicates you'll recognize precisely just how much your payments are and when you'll have to make them, allowing you to budget as necessary.

Degree term can be a wonderful option if you're looking to purchase life insurance policy coverage for the very first time. According to LIMRA's 2023 Insurance coverage Barometer Study, 30% of all adults in the United state requirement life insurance coverage and don't have any kind of kind of policy. Level term life is predictable and budget friendly, that makes it among one of the most popular sorts of life insurance coverage.

{kind=link}

Latest Posts

Low Cost Burial Insurance For Seniors

Advantages Of Funeral Insurance

Simplified Issue Final Expense Policy